Blockchain has made a huge buzz in the financial sphere over the last decade due to the astronomical profits that investors have seen in this period, especially those who have entered this space at an early stage.

It is worth mentioning that Blockchain is still in its nascent state, even though it is a decade-old technology. Many have compared Blockchain in 2018 as being similar to the Internet back in 1994 which implies the space is ripe for entrepreneurial pursuit.

From legal to banking to financial services and supply chain management, blockchain has a very wide range. So let’s explore more what Blockchain is.

What is a blockchain or a distributed ledger technology (DLT) network?

First introduced as an accounting system or ledger to store transactional data in the Bitcoin peer-to-peer network, a blockchain is a shared distributed database used to record transactions or account balances for a set of assets and users. It is a constantly growing list of linked ‘blocks’ or sets of chronologically ordered transactions that are time-stamped and linked together via special cryptographic functions. The ledger is ‘append-only’: data can only be added to the blockchain in sequential order. Once data is added to the blockchain, it is virtually impossible to alter it.

The features of blockchain

In contrast to traditional financial accounting systems, a blockchain ledger is not managed by any particular body or authority. Every member of the network holds a copy of the entire database/ledger and the ‘append’ (write) operation on the ledger is approved by the whole network in an automated and democratic way, without the need for a trusted third party (such as a bank). The orchestration of the system is dictated by the programmed scripts embedded in the protocol in a transparent and auditable way.

In effect, a blockchain is an ecosystem consisting of a data structure and ‘consensus mechanisms’ that ensure that parties interacting to share a common ‘state of truth’ regarding current and past transactions. This state of truth facilitates further interactions in a transparent and streamlined manner.

Why is blockchain important?

Blockchain’s importance lies in its unique combination of properties. These are:

- Decentralisation: There is no single point of trust and thus no single point of control.

- Auditability: Network participants can verify records directly, without external querying.

- Finality: There is only one ‘truth’ regarding what is happening and has happened in the ledger.

- Accountability: All actions can be traced to the person who initiated them and are recorded on the ledger.

- Direct trust: Unknown (and untrusted) parties can operate without the need for third-party intermediation.

- Elimination of single point of failure: No central authority or intermediaries are needed to oversee transactions. A copy of each ledger is stored and maintained by each node of the network.

- Security: Strong cryptographic ‘primitives’ (well-established, low-level cryptographic algorithms) are deployed to secure the network and the ledger.

- Transparency: The ledger can be public and maintained by all nodes of the network.

- Immutability: It is not possible to change any record on the ledger due to cryptographic ‘sealing’ via irreversible hash functions.

- Reliability: The ledger is resistant to outages and manipulation.

- Automation via smart contracts: Terms and conditions that underpin contracts can be encoded on the blockchain.

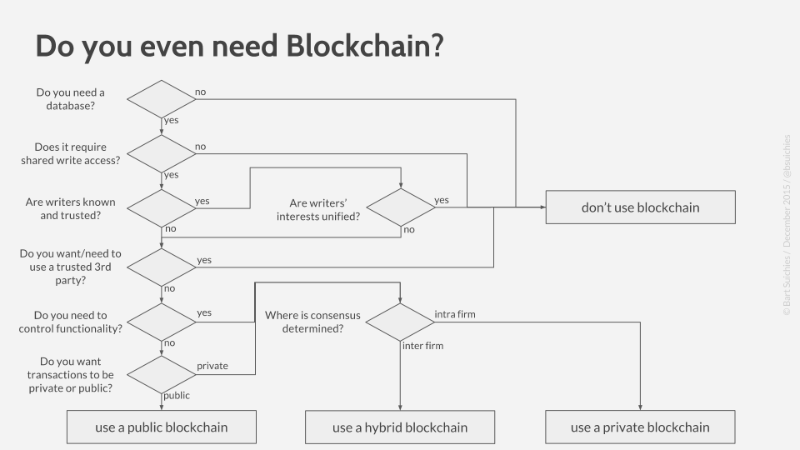

Deciding when to use blockchain

Before deciding whether blockchain is needed for a particular project or application, you need to decide whether the technology will actually add value to your current system. You can do this using the flowchart below. This guides you through the key issues to be addressed before using blockchain for your application. The main questions are:

- Is decentralisation really necessary?

- Are the nodes of the ecosystem trusted or untrusted?

- Are the nodes aligned or not?

- Is shared ‘write’ access required?

- Is a third party necessary for the application?

- Does the transactional data need to be public?

- Are the criteria governing whether a transaction is deemed valid known?

What are the moving parts in a blockchain?

Blockchain is a very complex technology as it is the product of multiple disciplines, including cryptography, systems engineering, distributed systems, economics and game theory. Before using the technology, you need to understand its ‘moving parts’ and how these will be applied in your application. The major moving parts are:

- Ecosystem roles: You need to understand the role of each stakeholder in the ecosystem and assign permissions and properties accordingly.

- Data structures: You also need to understand what is going to be written in the blockchain. Since this data structure will be used across all the stakeholders of the Blockchain ecosystem it has to be as standardised as possible.

- Consensus algorithms: You need to understand how a decision is taken in the ecosystem according to defined roles. Consensus algorithms enable a ‘state’ to be updated securely according to specified state-transition rules. The ability to carry out a state transition is distributed among users, who are collectively accorded the authority to perform a transition via an algorithm. The consensus protocol sets rules on how blocks are added to the chain, when blocks are considered valid, and how conflicts of truth are resolved.

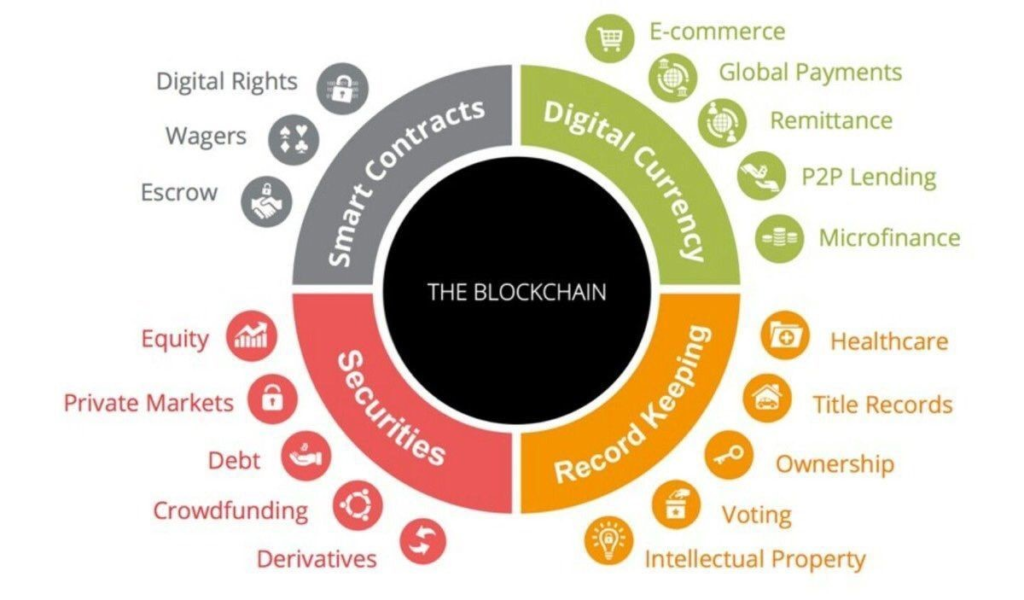

Potential applications for the start-ups of the future

Blockchain is still a very new technology and its applications are numerous. These include:

- Payments: Blockchain technologies are connecting global financial systems so they are easily interoperable, efficient, affordable and accessible. This can reduce the cost and time of cross-border payments. Confidence in blockchain technologies is rising as more governments and businesses invest in these areas.

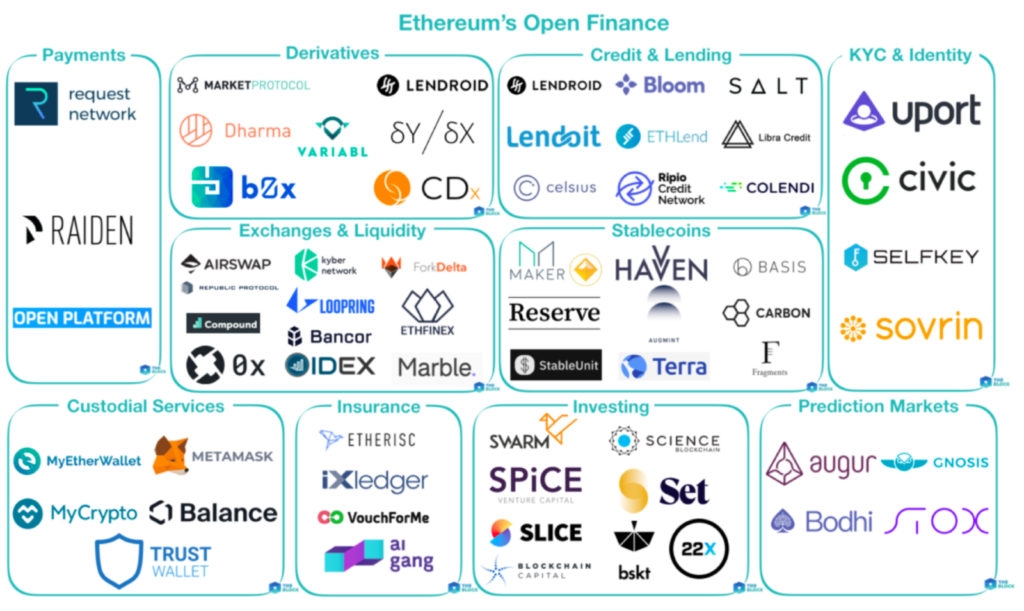

- Lending and other financial products: Decentralised finance (DeFi) is an emerging space that aims to reshape the financial industry using blockchain technology so that it is more transparent and auditable.

- Paper-based operations and title records: Blockchain has the potential to turn processes that are heavily reliant on physical record-keeping into a ‘paperless paradise’. Here, all parties to a transaction using blockchain and smart-contract technology would perform physical transactions, exchange and store information in an encrypted format, perform their contractual obligations, give and accept instructions, and exchange payments securely. Experts expect that most paper certifications, such as academic qualifications and birth certificates, will be validated through blockchain in the near future as it is the only way to fully eliminate forgeries.

- Intellectual property (IP): Digital signatures can be deployed using blockchain to establish ownership of IP in a way that cannot be challenged or refuted as all records are chronologically stamped and auditable in the ledger.

- Crowdfunding and financing new ventures: Blockchain can be used for financing new ventures via the ‘tokenisation’ method. Tokenisation is a method used for chunking any type of asset (e.g. real estate, equity, etc) into digital units as small as desired, giving the opportunity to fractional ownership by a wide range of investors. This has the potential to provide more cash liquidity to the startup industry (although tokenisation requires the establishment of proper regulatory and legal systems in the relevant country).

- Supply chain and logistics: Some interesting projects are currently underway that combine RFID and other sensor technologies with blockchain in order to streamline supply chains. RFID tags make use of electromagnetic fields to identify objects, and scanning an RFID tag provides the user with a host of useful data. (For example, it is easy to identify the product’s starting location, current location, and who has handled it.) The data associated with each item is stored on a blockchain that ensures accuracy and instant verification. The technology behind these projects provides reliable anti-counterfeiting via RFID identification; accurate product tracking and verification; improved security; and improved management and evaluation of processes.

- Traceability of high-value goods: Blockchain records the journey of goods across the supply chain from origin to destination and everywhere in between. This can facilitate compliance with standards and laws, and increase consumer trust. The ability to trace items is one of the most logical uses of blockchain. For high-value items such as pharmaceuticals, electronics and designer wear, blockchain is a solution to the traceability problem since it enables a single version of the truth; an immutable database of the history of goods from product to sale.

- Decentralisation and shifting from Web 2.0 to Web 3.0: Blockchain and cryptocurrencies such as Ethereum allow the building of web applications in a decentralised way. This means that applications can be developed in such a way as to reward creative actors, such as content creators, for their ‘creations of the mind’.

Watch: Entrepreneur’s Journey series – Blockchain for non-techie entrepreneurs

About Author: Dr. Theodosis (Theo) Mourouzis is a cryptologist and information security professional with strong interests in both academia and industry. He holds a BA/MA in Mathematics and an MSc in Pure Mathematics from the University of Cambridge, an MRes in Security Science and a Ph.D. in Information Security with Specialisation in Cryptography from University College London. He was the first recipient of the UK Cyber Cipher Security Challenge in 2013.

Theo is Managing Partner of Electi Consulting, a consultancy specialising in Blockchain, Cryptography and Artificial Intelligence. He is also an Industry Associate at UCL Centre for Blockchain Technologies and an Expert in Residence at the Institute of Innovation and Entrepreneurship at the London Business School.

He has extensive experience (10 years + ) working with governments, leading companies and organisations Lloyds Bank, US Navy, MSC Shipmanagement, Technology Strategy Board (TSB), Centre for Defence Enterprise (CDE), European Central Bank (ECB) and many others in the Blockchain space. He advised the Cyprus government in regards to the National Blockchain strategy and held a position at European Blockchain Partnership Initiative organised by the European Commission advising on technical aspects of the technology. He is also acting as Blockchain technical expert for the European Commission in regards to Blockchain projects.