Cringe-making, toe-curling, awkward, confusing, arrogant, shabby, disorganised, unbelievable, deluded … all words that could be used to describe the worst business pitches. And most of us have been there, at one side of the table or another. If you want to avoid pitfalls with pitches, then read on.

First up, I don’t consider myself to be a ‘pitch guru’. However, over the years, I spent some time in the vibrant London startup ecosystem, and have mentored startups in the UK and across the channel.

I come across pitches a lot – and I’m usually in the audience or watching from the wings. Sometimes it’s on a one-to-one, confidential basis. Other times, it’s at so-called pitching events.

This experience prompted me to clarify some thoughts about pitching. I haven’t provided any ‘general rules’. But this article might prove helpful as a checklist when you’re preparing your next pitch. These points are based on what I’ve heard before at pitches, time and again.

Five things you need in a pitch – but what’s often said:

1. What you do

If you can’t articulate what you do in a pitch to potential investors, partners or others, then how will customers have a chance of understanding? Be very clear at the outset. You should be able to give anyone a good idea within 30 seconds.

2. Unique selling proposition (USP)

What makes you different? Why does the marketplace need your products or services? Three reasons are ideal. Make them clear, compelling and unique. And show that you know the TLA! That’s a three-letter acronym standing for ‘three-letter acronym’! 😉

3. Competitors

Unless you’ve designed the world’s first teleportation machine or pizzas that deliver themselves, then you will surely have competitors. But even in that case, you have substitutes or competing technology, maybe from adjacent industries (for some time, the bicycle would be a competitor for teleportation to me!). The answer above is naive. Prepare for this question. Research competitors, even if their offering is slightly different. Know their strengths and weaknesses. Work out if your advantages are sustainable.

4. Your team

So many people respond this way. But we are all unique in some way. This kind of answer also points to a slightly unhealthy inward-looking approach to the business that could be viewed as self-serving. Much better to explain the business benefit of each individual, which might be their experience, contacts, etc. Then your ‘stock’ will grow in their minds of investors. After all, they are investing in your team. So why should they?

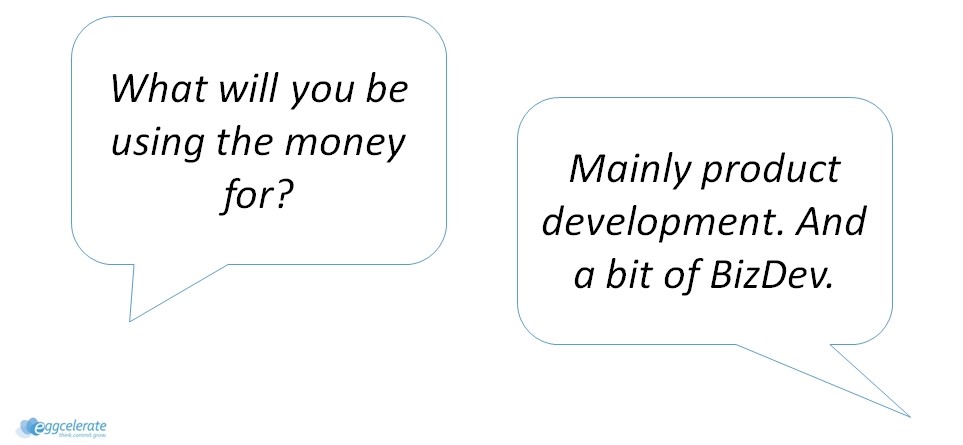

5) Finance

This is where many pitches come unstuck. Until now you’ve been talking about ‘your world’. Now you’re firmly in their territory. And they are the experts. Make sure you have the right answers and figures to back up everything you say – otherwise your pitch will unravel at this point (if it’s still intact). Be detailed about what you’re using the money for. Use an expert to help you with this – so you’re confident in all you say.

Other points

There are plenty more I could add which are essential too: Liabilities, trademarks/patents, working capital, return on investment, and exit strategies, to name a few.

Then we could get into all the detail beneath each of these, which is crucial because your audience may push you for more information. The conversation could take all sorts of twists and turns. But each pitch will be so unique for every company that a single article can’t do the job.

Parting advice

I have mentored many startups in different sectors (IT, Drones, IoT, Insure/FinTech, Incubator, and more). But when it comes to pitches, many of the ground rules are exactly the same, and they all need to work towards answering a single question: Is this a viable business worth investing in?

What I hope you’ll take from this article is the need to be 100% prepared for your next pitch. Work with someone who will give you clear, honest and constructive feedback. Much better to take it from them and work together on making it better, than emerging from a pitch with your dream in tatters and a potentially brilliant business plan that’s failed at the first hurdle.

About the author: Stefano Maifreni

An engineer by education, product manager by role and expert at achieving growth by career, Stefano has an outstanding track record in strategy, operations, product and business development, with extensive P&L management and international expansion experience.

His professional journey includes Senior Manager roles in global Blue-chip companies, Growing Businesses and Startups in technology-intensive and innovative industries (IT, Technology Manufacturing, Drones, IoT, Insure/FinTech, Immersive Theatre).

Stefano is an Executive MBA graduate of the London Business School, a published author (Forbes, The Guardian, and various SME-focused publications), and a regular speaker and moderator at AI-, IoT- and Blockchain-related events in London and Milan.

In 2014, he founded Eggcelerate to help Founders of ambitious B2B start-ups gain a position in the market and deliver upon investors’ expectations from post-seed to Series-A.

(Main image credit: Photo by Photo Boards on Unsplash)