The global personal luxury goods market has nearly tripled in profits over the past five years, driven by megabrands, digital innovation, and heritage products, yet challenges like brand fatigue, pricing scrutiny, and sustainability concerns are reshaping the industry. In this article, Neha Reddy explores the luxury goods market outlook, LVMH’s growth trajectory through a private equity lens, and a comparative analysis with Kering, revealing what defines success for luxury brands in a shifting market.

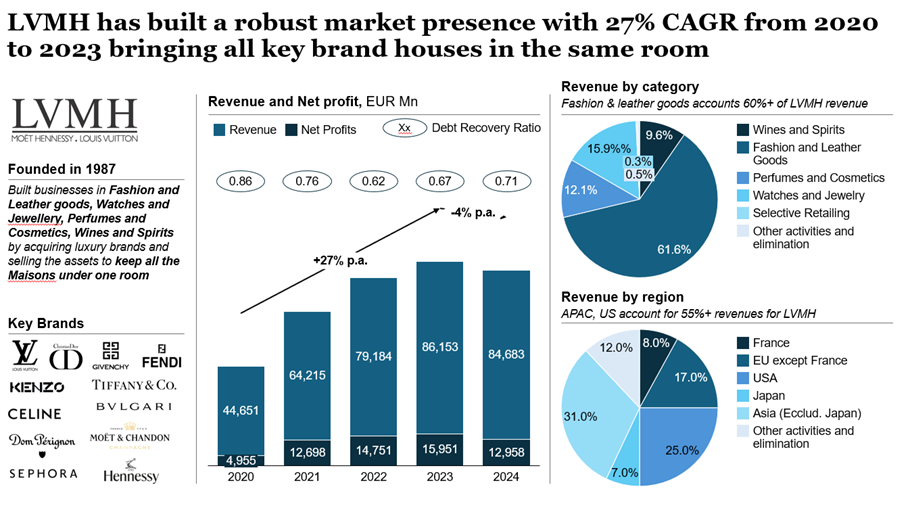

The ever-changing environment tests even the most established brands. LVMH (Moët Hennessy Louis Vuitton SE), a French multinational holding company and conglomerate that specializes in luxury goods valued at over $400 billion, dominates the industry through a private equity–style acquisition and integration model that has built an unmatched portfolio. Its diversified structure has shielded it from the volatility that has challenged peers such as Kering, which remains heavily dependent on Gucci.

The luxury brand market: growth and structural shifts

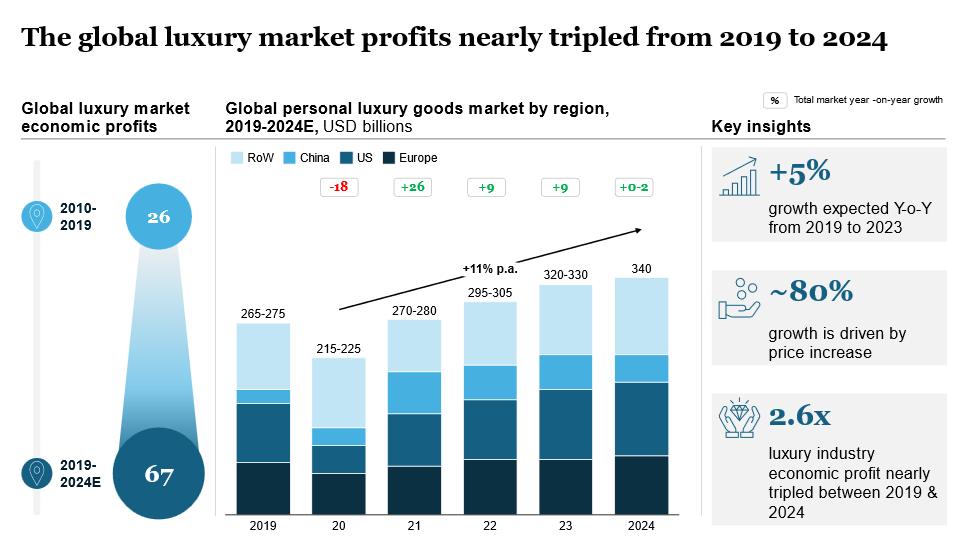

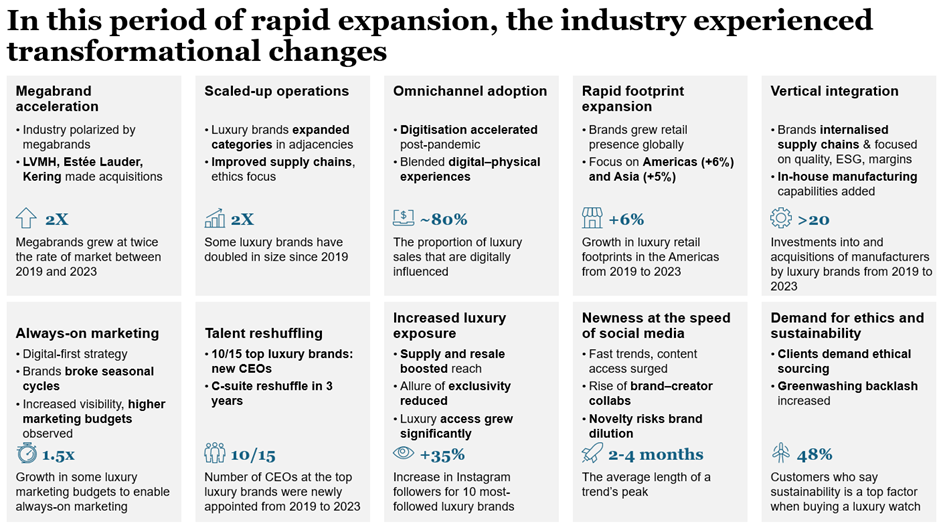

Between 2019 and 2024, the global personal luxury goods market grew at an ~11% Compound Annual Growth Rate (CAGR)1, with profits nearly tripling1. China (+26%)1 and the U.S. (+9%)1 led regional growth, while Europe remained largely flat. Megabrands, including LVMH, Estée Lauder, and Kering out-performed the broader industry, doubling in size through scale, global retail expansion, and the adoption of omnichannel strategies.

The market has also being reshaped by several structural trends:

- Digital-first strategy: Brands moved beyond traditional seasonal cycles, adopting always-on campaigns, and leveraging influencer and creator collaborations.

- Omnichannel retailing: Physical and digital experiences became blended, while resale platforms and direct-to-consumer initiatives widened reach.

- Vertical integration: In-house manufacturing and supply chain ownership improved margins, quality, and ESG control.

- Sustainability and ethics: Today, approximately 50% of luxury clients consider sustainability to be a top purchase factor, increasing scrutiny over sourcing, craftsmanship, and brand transparency.

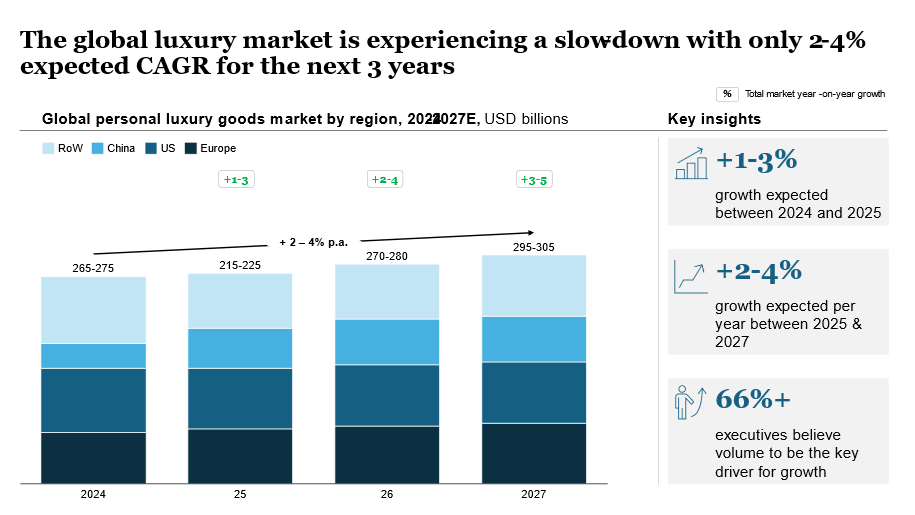

Despite these gains, the industry faces headwinds. Growth is projected to moderate to 2–4% CAGR from 2024–27.

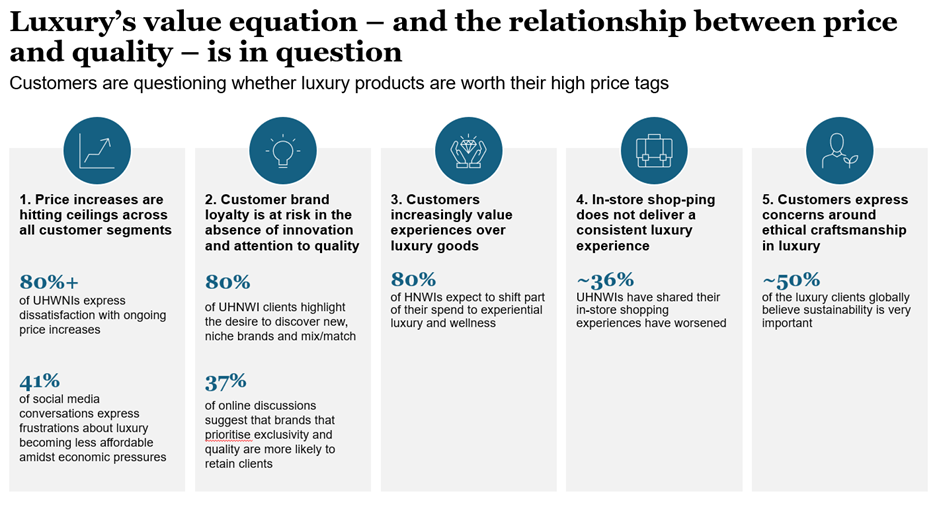

Consumers are increasingly questioning price-value equations: 80%+ of ultra-high-net-worth individuals express dissatisfaction with relentless price hikes, and ~41% of social media discussions voice frustration about affordability.

LVMH’s strategy: private equity in luxury

LVMH’s approach illustrates how a strategic, disciplined, and diversified model can sustain growth. Its dominance in the luxury brands sector is rooted in a strategy that mirrors private equity investing. Bernard Arnault, Chairman and CEO of LVMH and the architect of its modern form, entered the luxury industry in the 1980s through the acquisition of the bankrupt Boussac Saint-Frères, whose jewel was Christian Dior. It was a textbook distressed buyout: assume liabilities, isolate world-class assets, and rebuild value. Dior became the foundation on which Arnault constructed a platform.

The consolidation of Louis Vuitton with Moët Hennessy in 1987, followed by leveraged share purchases to secure control by 1989, effectively mirrored a leveraged buyout, amplifying his equity through debt, similar to how private equity sponsors maximise returns.

Over three decades, Arnault executed a buy-and-build strategy: acquiring and integrating complementary houses such as Fendi, Bulgari, Sephora, Tiffany & Co., expanding across fashion, jewellery, cosmetics, and wines and spirits.

These bolt-on acquisitions were financed not only through new borrowing but through disciplined recycling of cash flows from revitalised brands: Dior’s turnaround funded early growth, while Louis Vuitton’s global expansion provided the capital for further deals. This strategy allowed Arnault to control assets far beyond his personal equity stake, compounding LVMH’s scale in a manner strikingly similar to how funds build portfolios. Portfolio diversification and disciplined capital allocation are central to avoiding volatility and brand fatigue.

Maintaining brand identity while scaling

What differentiates LVMH is the balance between operational discipline and brand autonomy. Arnault’s stewardship adapted the private equity toolkit to the unique dynamics of luxury brands. Governance discipline, financial oversight, operational improvements, and marketing innovation were all hallmarks of his approach. Yet, unlike typical private equity roll-ups that centralise operations, he preserved the creative independence of each Maison, allowing Dior, Fendi, and Bulgari to retain their distinct identities while benefiting from group’s shared resources and scale. The repositioning of Tiffany into high-end jewellery or Sephora’s rapid international rollout are examples of operational excellence applied with a long-term lens.

A long-term view: building value beyond the exit

The key divergence from private equity lies in the time horizon. Whereas funds operate within seven-to-ten-year cycles and face constant pressure to exit, Arnault has employed permanent capital – with no obligation to sell, only to grow.

This long term view has enabled investments in heritage, artisanship, and cultural sponsorships that would rarely survive under short-term ownership. Yet the similarities to private equity remain unmistakable. Platform creation, bolt-on acquisitions, leverage, and operational discipline have all shaped LVMH into a market leader. In many ways, LVMH stands as a case study to demonstrate how the private equity playbook, applied with patience and creativity, can build not just financial value but an enduring corporate dynasty.

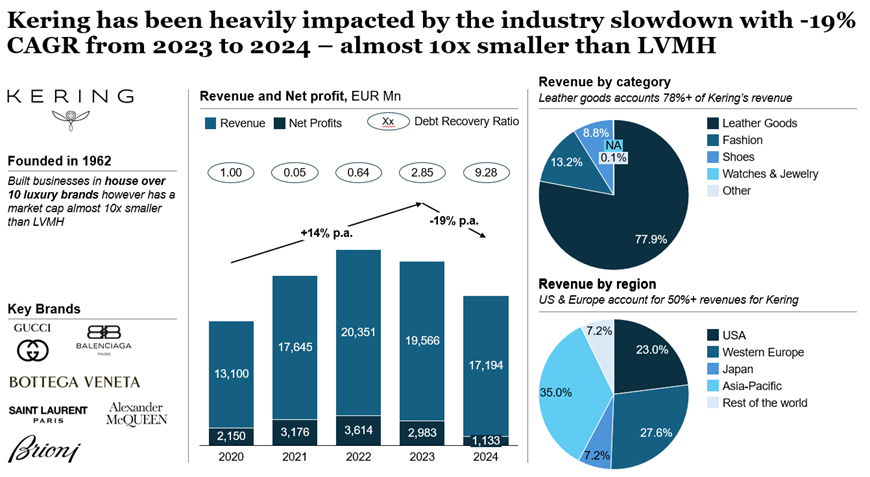

Kering: the risks of concentration

Kering offers a cautionary contrast to LVMH’s diversified model. Despite its strong portfolio, the group remains heavily dependent on Gucci, which generates around 78% of total revenues. This concentration has exposed Kering to brand fatigue and cyclical downturns, contributing to a -19% CAGR between 2023 and 2024, compared with LVMH’s +27% growth over the same period.

Attempts to diversify through Bottega Veneta, Saint Laurent, and Balenciaga have brought only partial relief. These brands, while distinctive, have yet to reach the scale or resilience of LVMH’s Maisons. The result is a portfolio that remains vulnerable to shifts in consumer sentiment and lacks the operational diversification and acquisition discipline that underpin LVMH’s success.

Sustaining leadership in a slowing market

The coming years will test the resilience of luxury houses. Even as jewellery and leather goods remain resilient, overall market growth is slowing, and consumers are more discerning than ever. Today’s luxury clients expect more than premium products. They seek authentic craftsmanship, innovation, immersive experiences, and visible commitments to ethics and sustainability. About 80% of high-net-worth individuals expect to shift a portion of their spending to experiential luxury and wellness, while ~36% of ultra-wealthy clients report worsening in-store experiences.

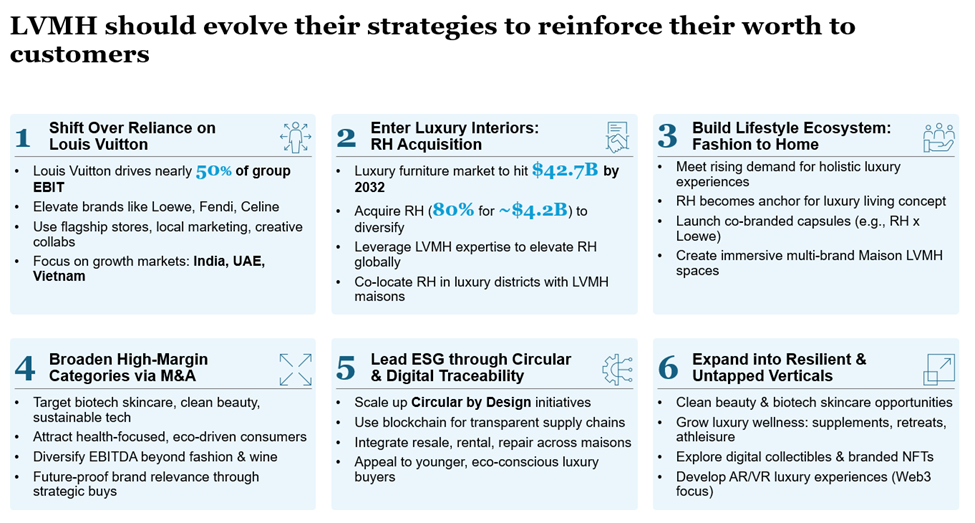

For LVMH, the implication is clear: the private equity-style playbook that drove expansion must now be complemented by a stewardship approach that sustains relevance. This means balancing financial rigour with creativity, heritage, and cultural authenticity.

To respond to shifting expectations, LVMH and other luxury brands are focusing on four strategic levers: sharpening the core brand proposition, renewing emphasis on product excellence, enhancing customer experiences, and carefully evaluating expansion opportunities. Success will increasingly be defined not by pricing power alone, but by the ability to deliver enduring value beyond the product itself.

The road ahead

LVMH is already well-positioned to sustain leadership because its portfolio diversification insulates it from reliance on any single brand. Yet the sustainability of its advantage will depend on whether it can balance financial discipline with authenticity and cultural stewardship. As price-driven growth reaches its limits, the future will be defined by how convincingly LVMH and its peers reinforce value beyond the product—through heritage, ethics, and unforgettable experiences.